Higher Education Rating Agency Medians – Some Stabilization in FY 2023, but Enrollment and Operational Challenges Remain

Operating Performance Softens Across Sector, Though Rising State Support Provides a Buffer for Publics

For public universities, however, increased state funding provided a welcome steadying factor for operating performance given the other challenges facing the sector. Moody’s indicated that over half of their rated publics saw state appropriations per student increase by 9% or more in FY 2023, and state appropriations per FTE (“full time equivalent”) increased across S&P’s rated universe of publics by 11.6%. Although growth in appropriations has not been, and isn’t expected to be, perfectly consistent across all states (with S&P noting cuts to higher education budgets in Arizona and California announced for FY 2025), rating agencies expect continued strong support from state governments overall. Such support will continue to increase revenue diversity for publics while helping to ease expense and demand-based pressures on operating performance.

Relative Enrollment Stability, But Lower-Rated Universities Face Greater Pressures

The Federal Reserve’s fight against inflation and its impact on markets and the broader economy remain key issues. In recent weeks, we have seen encouraging data suggesting that inflation is finally falling back toward the Fed’s long-term 2% target. In June, the core personal consumption expenditures price index, the Fed’s preferred inflation gauge, increased 0.2% and was up 2.6% from a year ago. A jobs report released earlier this month showed unemployment rising to 4.1%, slightly higher than the 4% target set by the Fed. Debt and equity markets have been reacting favorably to the news. According to the CME Group, as of July 30 there is now a 100% probability of a rate cut on or before the September 18th meeting. 85.8% of respondents believe there will be a 25 bps cut, while just under 14% of respondents believe it will be a 50 bps cut. Many of those respondents think further cuts will be in store before the end of the year. As of July 30, ~57% of those surveyed believe the fed funds rate will be in the 450-475 bps range following the December 18 meeting.

Wealth Levels Remain Stable, With Market Factors Driving Capital Spending and Reduced Debt

Information in this article has been drawn from the following median publications from Moody’s, S&P, and Fitch.

[1] “Higher Education – US: Medians – Private Universities’ Revenue Rebound Slows While Inflation Continues,” published May 6, 2024 by Moody’s.

[2] “Higher Education – US: Medians – Public Universities’ Operating Performance Softens As Pandemic Aid Ends,” published June 6, 2024 by Moody’s.

[3] “U.S. Not-For-Profit Public College and University Fiscal 2023 Medians: Rising State Funding Offers Hope Amid Continued Demand Pressures,” published July 18, 2024 by S&P.

[4] “U.S. Not-For-Profit Private College and University Fiscal 2023 Medians: Inflated Expenses, Deflated Support Contribute To Weaker Margins,” published July 18, 2024 by S&P.

[5] “Fiscal 2023 Median Ratios for U.S. Not-for-Profit Private Colleges and Universities: Tuition Growth Insufficient to Preserve Margins,” published July 2, 2024 by Fitch.

[6] “Fiscal 2023 Median Ratios for U.S. Public Colleges and Universities: Stabilized Post-COVID Performance,” published July 26, 2024 by Fitch.

Comparable Issues Commentary

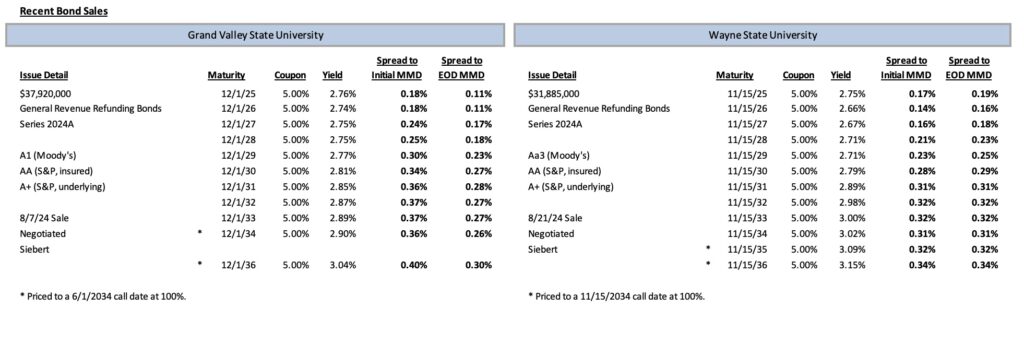

Recent Bond Sales

| Issue Detail | Maturity | Coupon | Yield | Spread to Initial MMD | Spread to EOD MMD |

|---|---|---|---|---|---|

|

$37,920,000 General Revenue Refunding Bonds Series 2024A A1 (Moody's) AA (S&P, insured) A+ (S&P, underlying) 8/7/24 Sale Negotiated Siebert |

12/1/25 | 5.00% | 2.76% | 0.18% | 0.11% |

| 12/1/26 | 5.00% | 2.74% | 0.18% | 0.11% | |

| 12/1/27 | 5.00% | 2.75% | 0.24% | 0.17% | |

| 12/1/28 | 5.00% | 2.75% | 0.25% | 0.18% | |

| 12/1/29 | 5.00% | 2.77% | 0.30% | 0.23% | |

| 12/1/30 | 5.00% | 2.81% | 0.34% | 0.27% | |

| 12/1/31 | 5.00% | 2.85% | 0.36% | 0.28% | |

| 12/1/32 | 5.00% | 2.87% | 0.37% | 0.27% | |

| 12/1/33 | 5.00% | 2.89% | 0.37% | 0.27% | |

| 12/1/34* | 5.00% | 2.90% | 0.36% | 0.26% | |

| 12/1/36* | 5.00% | 3.04% | 0.40% | 0.30% | |

| *Priced to a 6/1/2034 call date at 100%. | |||||

| Issue Detail | Maturity | Coupon | Yield | Spread to Initial MMD | Spread to EOD MMD |

|---|---|---|---|---|---|

|

$31,885,000 General Revenue Refunding Bonds Series 2024A Aa3 (Moody's) AA (S&P, insured) A+ (S&P, underlying) 8/21/24 Sale Negotiated Siebert |

11/15/25 | 5.00% | 2.75% | 0.17% | 0.19% |

| 11/15/26 | 5.00% | 2.66% | 0.14% | 0.16% | |

| 11/15/27 | 5.00% | 2.67% | 0.16% | 0.18% | |

| 11/15/28 | 5.00% | 2.71% | 0.21% | 0.23% | |

| 11/15/29 | 5.00% | 2.71% | 0.23% | 0.25% | |

| 11/15/30 | 5.00% | 2.79% | 0.28% | 0.29% | |

| 11/15/31 | 5.00% | 2.89% | 0.31% | 0.31% | |

| 11/15/32 | 5.00% | 2.98% | 0.32% | 0.32% | |

| 11/15/33 | 5.00% | 3.00% | 0.32% | 0.32% | |

| 11/15/34 | 5.00% | 3.02% | 0.31% | 0.31% | |

| 11/15/35* | 5.00% | 3.09% | 0.32% | 0.32% | |

| 11/15/36* | 5.00% | 3.15% | 0.34% | 0.34% | |

|

*Priced to a 11/15/2034 call date at 100%. 1Spreads to AAA MMD are based on end-of-day uninterpolated MMD on the day of pricing for each issue. |

|||||

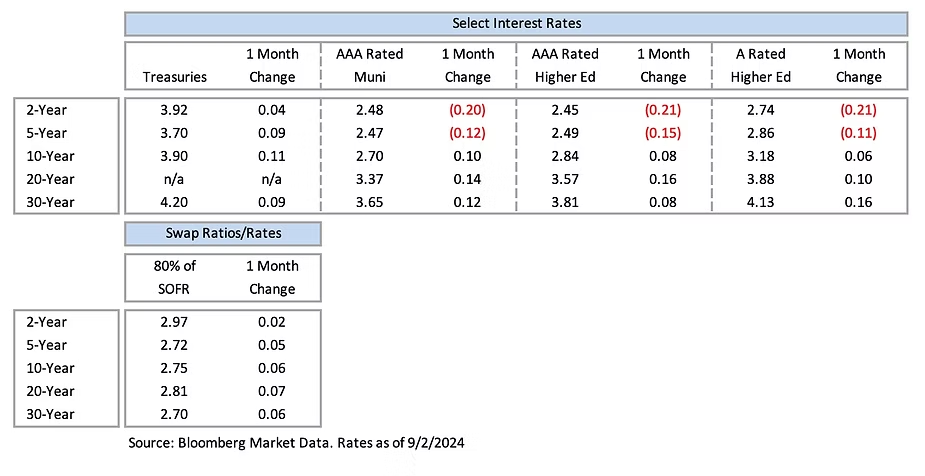

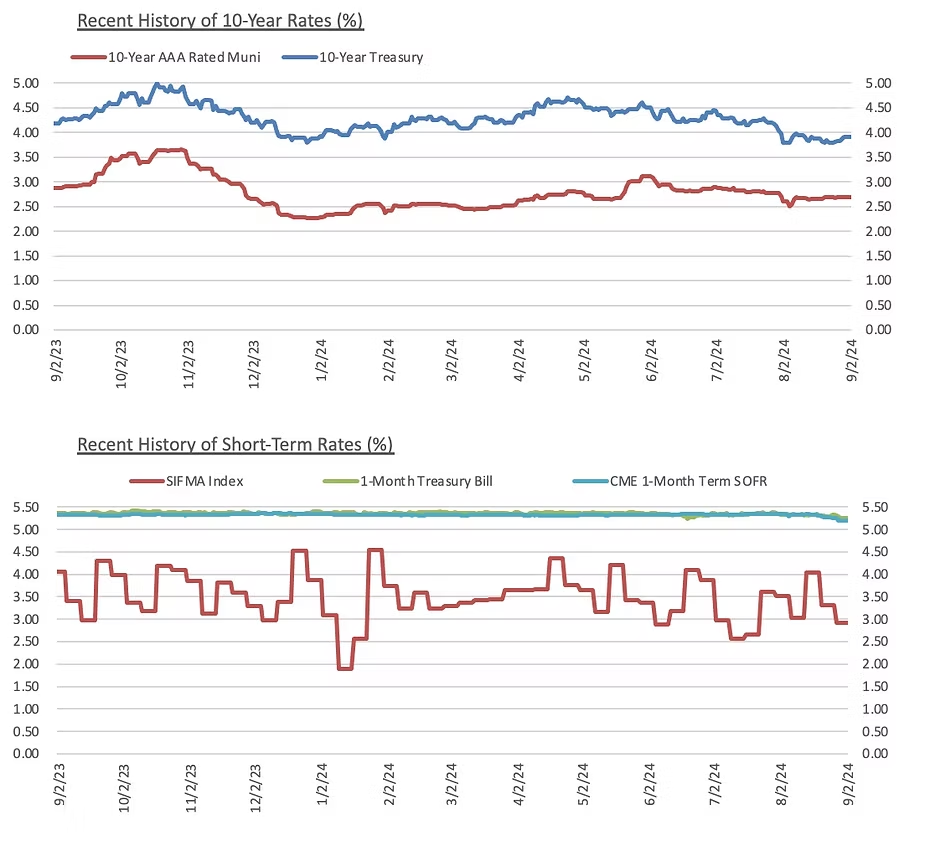

Interest Rates

Meet the Author:

Maxwell Wilkinson | mwilkinson@blueroseadvisors.com | 952-746-6048

Media Contact:

Laura Klingelhutz, Marketing Coordinator

952-208-5710