Existing Trade Strategies

Changes in regulations, market conditions, interest rates, and even the status of a counterparty can affect the position of an existing derivative. Blue Rose provides ongoing review of our clients’ hedging instruments to evaluate the risk/reward of each position and to offer recommendations for a change, if warranted.

Swap Restructuring Through an Interest Rate Blend and Extend

Existing interest rate swaps can be restructured many ways. One restructuring strategy used for swaps executed in higher rate environments is to “blend and extend” the swap. In a lower interest rate market, the maturity of the original swap is extended by a few years, which lowers the rate. The negative market value of the existing swap is rolled into the new swap, and the rate may still be significantly lower based on how much rates have moved. The blend and extend strategy is effective for certain borrowers because it can lower the interest payments in the short term and it can provide interest rate protection beyond the original maturity date of the swap.

If you are considering using a blend and extend strategy for existing higher rate derivatives, Blue Rose can help you make sure the proposed restructuring is priced appropriately and meets your cash flow needs.

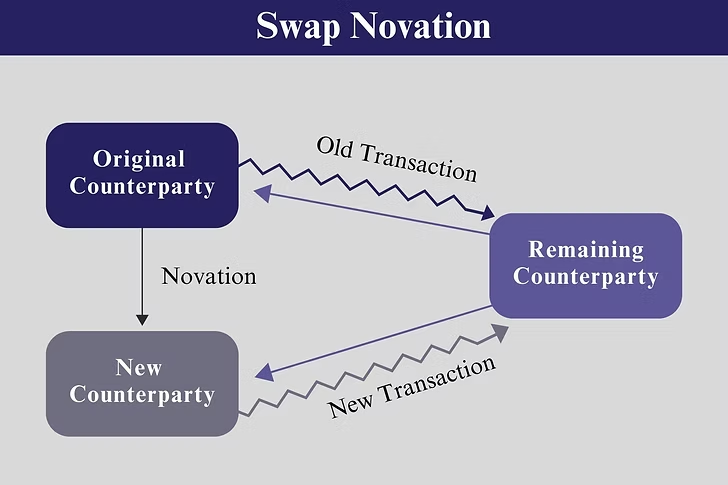

Partial and Full Swap Novation

In a swap novation, the rights and obligations of the original bank counterparty are replaced by a different bank counterparty and a new transaction is created with identical terms to the old transaction, except where agreed upon between the parties and evidenced by a novation confirmation. In addition, the transaction between the new counterparty and the remaining party can be modified to reflect new credit and/or economic terms through a new confirmation. An essential component for a successful novation is having the written consent of all parties. The decision to execute a partial or full novation can be motivated by a need to replace an existing counterparty, a desire to create counterparty diversification, or as a collateral mitigation strategy. Partial to full swap novation can be accomplished at no cost or at marginal incremental costs. For collateral mitigation strategies, released collateral can be invested in less restricted investments for higher returns and a positive overall transaction internal rate of return.

Partial and Full Terminations

A partial termination is the reduction in the notional amount of a swap/derivative contract. A party to an interest rate swap contract can negotiate a reduction in the swap’s notional amount for the remaining payment dates with the other party. All other terms of the swap contract would remain the same. Such an action may create a realized gain or loss that would need to be accounted for in a given party’s financial statements. A full termination is the early completion of a swap contract. Both parties cease to make payments and the terminating party may be required to pay damages to the other. Changes in the shape of the yield curve, replacement strategies or monetization of profits can all be motivators for full or partial terminations of derivative position. Default events such as bankruptcy or failure to pay can also cause the early termination of a swap contract.