Generally, in a positively sloped yield curve environment, issuers benefit from investing the bond proceeds in their project funds by purchasing investments with a longer duration that offer a higher yield when compared with money market funds or other short duration instruments. In this manner, project funds are typically invested in Treasury or Agency securities, which are generally considered “risk free.” Currently, though, the yield curve is flat to inverted, so we often see longer duration investments earning comparable or even lower returns than shorter, more liquid investments. Because these common investment vehicles are perceived by the market to be “risk free,” they therefore offer little to no credit spread above the Treasury curve. Since the underlying Treasury yield curve is currently inverted, project funds with a longer duration earn no yield benefit over shorter duration instruments.

Repurchase agreements, or “repos”, are often viewed as “risk-free” investments as well, and therefore offer no additional yield for longer durations. Further, if a project fund amortizes, repos may have an even more inverted yield curve than laddered portfolios because the cost of holding the associated collateral is typically a flat fee per year. With a declining balance, the equivalent basis points in yield for the same flat fee would increase as draws are made.

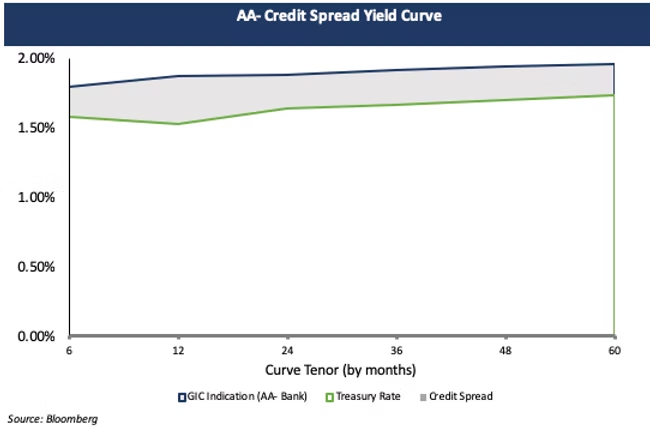

Unsecured guaranteed investment contracts, or “GICs”, are the only investment option for project funds that include a credit component, meaning that the yield does not directly correlate to the inverted treasury yield curve. An unsecured GIC will offer a positively sloped credit spread curve that can offset the negatively sloped yield curve based on the bank’s credit rating. Because it is attractive for banks to lock up funding for a longer amount of time, project funds with longer durations can actually earn a higher yield. For example, in the chart below, we show the approximate credit spread curve for a AA-rated bank, as well as the Treasury yield curve. As you can see, while the Treasury curve is inverted, when the bank credit curve is layered on top of this, the resulting funding curve is positively sloped.

We encourage you to reach out to your Blue Rose advisor to determine if you or your issuer’s project fund could potentially benefit from being invested in an unsecured GIC.

About the Author:

Georgina Walleshauser joined Blue Rose in April 2017. As an Analyst, she is responsible for providing analytical, research, and transactional support to senior managers serving higher education, non-profit, and government clients with debt advisory, derivatives advisory, and reinvestment services. She also prepares debt capacity modeling, credit analysis, and market analysis to support the delivery of comprehensive, strategic, and resourceful capital planning tools to our clients.