In the 90-plus days since COVID-19 interrupted the 2020 Spring term in an historically unprecedented fashion, the credit rating agencies have moved quickly to measure the pandemic’s immediate and prospective impact upon higher education institutions across the country. On March 18, Moody’s changed its outlook on the higher education sector from “stable” to “negative,” joining Standard and Poor’s and Fitch. who both began the calendar year with negative outlooks on the sector.

In the ensuing pandemic response period, the rating agencies have released periodic sector commentary, research, and rating action updates (links to many of those publications are provided below). The rating agencies have also conducted interactive webinar events to present research and respond to questions. In the bullets below, we have summarized some of the key takeaways from these recent sector commentaries:

Almost all sources of higher education revenue are expected to decline as a result of the economy-wide impact of COVID-19:

State appropriations (falling state revenues will lead to budget cuts for higher education, primarily for public institutions but also for privates who receive state grants)

Auxiliary revenue (refunds for housing, dining, and activity fees will affect FY20 results and revenues likely will be strained for FY21, as reopened campuses are forced to operate with social distancing requirements)

Net tuition (a weaker economy and aggressive competition for students will increase tuition discounting while alternative learning formats such as online-only will reduce prices students are willing to pay for instruction)

Endowment income (declines in asset values and lower returns from a weaker economy will put significant pressure on endowment draw rates)

Gifts (philanthropy will be reduced for reasons similar to the endowment challenges)

Grants and contracts (while federal government grants may continue, grants from states and the private sector will decline).

Expenses will grow in the immediate term and decline over time as institutions react to falling revenues and reassess spending, although expense reduction will lag behind revenue shortfalls.

Institutions with sound financial operations prior to COVID-19 may find opportunities for growth as weaker peers struggle under new challenges.

Institutions with demand debt and cash-strapped institutions looking to access liquidity facilities will be particularly vulnerable to overall capital market disruptions.

Federal and state government stimulus programs such as the CARES Act will provide immediate relief for lost or refunded revenue, but the impact may be short-term.

Higher unemployment may increase overall higher education enrollment, particularly for institutions with adult learning programs and robust online offerings.

Even if enrollment does increase, net tuition may decrease overall as student enrollment pivots to more affordable 4-year colleges and universities or community colleges, and as financial aid needs increase.

Institutions with significant full-pay foreign student enrollment may find net tuition challenges as they try to replace lost enrollment with domestic students paying in-state rates or expecting institutional aid.

While most institutions were able to successfully switch to online-only instruction in Spring 2020, an institution’s ability to offer on-campus learning in Fall 2020 will have a dramatic effect on student demand and the price students are willing to pay for instruction, not to mention the impact on student-driven revenues such as auxiliary revenue.

Lost revenue (and expense savings) due to limitations on athletic events may be relatively neutral for many institutions other than the largest football and basketball programs.

Despite the overall negative outlook on the sector and the evolving evaluation of the impact of COVID-19 on institutional credit ratings, to date there have been fewer than two dozen downgrades across the sector by all three agencies combined. While Standard and Poor’s did perform a blanket outlook change to “Negative” for 118 institutions (84 private, 34 public) on April 30 (see article link below), rating actions since March have largely been limited to new issue ratings, as rating agencies have taken more of a “wait-and-see” approach for institutions facing periodic surveillance updates. This acknowledges the reality that key information such as FY20 financials and Fall 2020 enrollment will not be available for most institutions until a few months from now. We expect that a more robust rating agency reaction to the impact of COVID-19 will not be felt until the fourth quarter of 2020.

The credit impact of COVID-19 will continue to evolve over the coming months. Blue Rose continues to be an advocate for the institutions we serve as they present their story to the rating agencies. Please reach out to a member of the Blue Rose advisory team if you have any credit rating related inquiries or questions. Be well and have a great summer.

Recent Rating Agency Publications

Moody’s (May Require User Login)

Higher education – US: Outlook shifts to negative as coronavirus outbreak increases downside risks (March 18)

Federal aid provides modest support for universities coping with coronavirus (April 1)

Coronavirus will lower student demand and increase costs for universities (April 7)

Coronavirus effects: Credit drivers and rating consequences Rating Actions March 1 – April 15 (May 1)

Largest debt issuers are well positioned to weather coronavirus shocks (May 12)

Even with potential enrollment gains, colleges face drop in tuition revenue (June 13)

Standard & Poor’s (May Require User Login)

Fitch (May Require User Login)

Comparable Issues Commentary

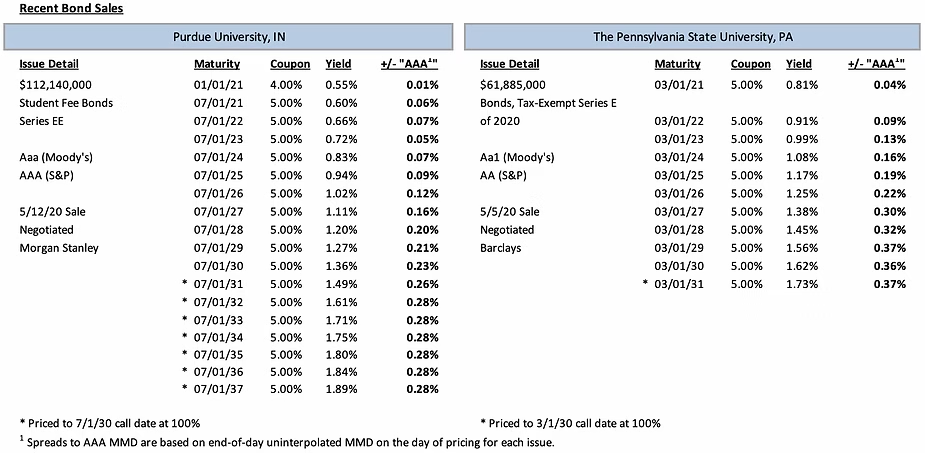

Shown below are the results of two negotiated, tax-exempt public higher education issues that sold in the month of May. Purdue University (“Purdue”) and the Pennsylvania State University (“Penn State,” or “PSU”) priced tax-exempt bond issues on May 12th and May 5th, respectively. While Purdue’s tax-exempt issuance was nearly double the size of Penn State’s ($112.14M vs. $61.885M), Penn State also concurrently priced a substantial taxable issue of over $1 billion on May 5th. Penn State’s Tax-Exempt Series 2020E Bonds were issued solely for refunding purposes, refinancing the University’s outstanding Series 2009B bonds. In contrast, while Purdue’s Series EE Student Fee Bonds did include a small refunding component for its outstanding Series Z-1 bonds, the majority of the issue was devoted to new money borrowing for two major projects – the University’s new Engineering and Polytechnic Gateway Building , and its Veterinary Medicine Teaching Hospital. Significant equity contributions comprising gifts and University funds will supplement bond proceeds as another source of funding for the two projects. Purdue’s bonds were rated Aaa/AAA (Moody’s/S&P), while PSU’s bonds carried ratings one to two notches lower at Aa1/AA (Moody’s/S&P).

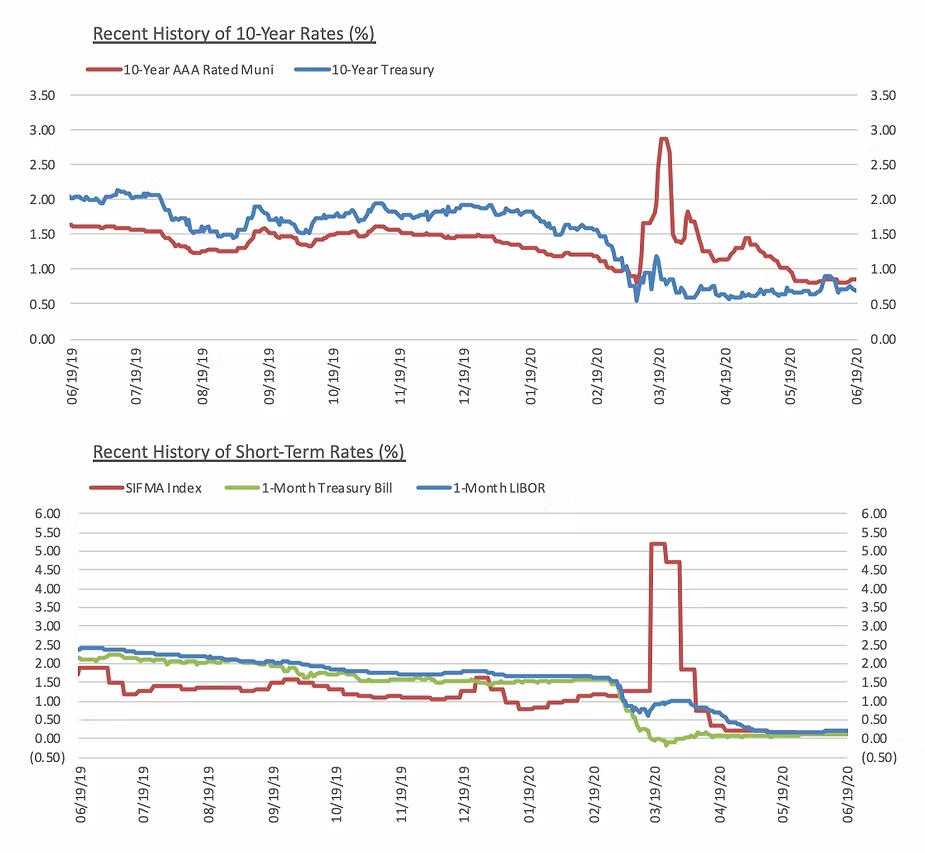

After a turbulent April in the municipal market, a month where the MMD index was unchanged or increased for 10 straight business days from April 17th to April 30th (resulting in increases of 0-40 bps across the curve), both Purdue and Penn State benefitted from a strong May rebound. Over the entire month of May, MMD fell or was unchanged at each point on the curve on every single trading day (falling 51-71 bps across the curve over the month), an unusually consistent trend of declining rates. This rebound paralleled an increase in investor demand for new tax-exempt issues, including for institutions of higher education. Although credit spreads remain wider than pre-pandemic levels (both Purdue and Penn State priced at spreads ranging from 10-25 bps wider than their most recent previous tax-exempt financings), the final 10-year spreads to MMD of 23 bps for Purdue and 36 bps for PSU were markedly tighter than those achieved by similarly rated higher education borrowers in the more challenging April market. Both transactions were fully serialized through their respective final maturities, although Purdue’s 2037 final maturity exceeded Penn State’s by six years. Coupon structure and call features for the two transactions were also nearly identical, with both schools selling almost exclusively 5% coupon maturities across the entirety of the curve and offering their issues with standard 10-year call features.

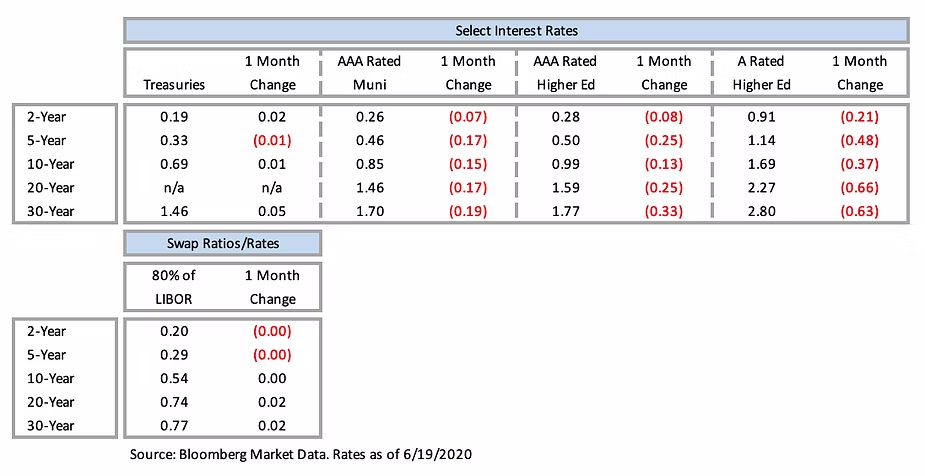

Interest Rates

About the Author:

James McNulty | Managing Director | [email protected]