Administrators across the country designed low density housing plans for the safe reopening of on-campus housing during the fall of 2021, including the numerous Public-Private Partnership (P3) housing projects in operation around the nation’s higher education institutions. But many, if not most, institutions came to understand that this just simply did not work financially. In this article, we highlight some of the financial implications for why lower occupancy does not work using a simplified example. The example provided below demonstrates that under lower occupancy scenarios, the University and/or their P3 partners needed to rely on University support or, if University support was not feasible, many projects needed to draw on reserve funds to make debt service payments. The example considers a basic generalized scenario to understand what happens/happened to the project’s financial performance under the lower-than-projected occupancy and is focused on addressing two basic questions:

- What would be break-even occupancy for a typical P3 undergraduate housing deal?

- What happens to the debt service coverage ratio and cashflow if a University decides to only have single person occupancy in each unit?

In answering these questions, we also discuss potential long-term implications for each scenario.

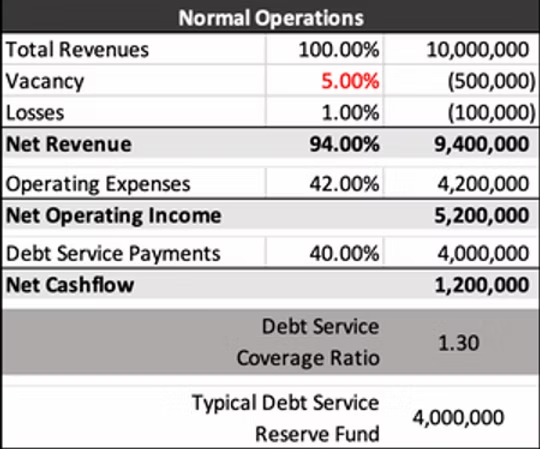

Scenario – Normal Operations

Consider a University P3 housing project that has 1,000 beds configured with occupancy as follows: 100 quad units (400 beds), 200 double units (400 beds) and 200 single units (200 beds); in total, the 1,000 beds are spread across 500 housing units. If we assume an average cost per bed of $10,000, the project has $10 million of revenue potential. Using an assumption of 95% occupancy (5% vacancy), other losses of 1%, and operating expenses of 42% of potential revenue, the project would have net operating income of $5.2 million. If debt service payments are 40% of potential revenue, then debt service payments are $4.0 million, leaving net cashflow of $1,200,000.

Based on the above parameters, the debt service coverage ratio (DSCR), which is equal to net operating income / debt service payments, would be 1.3x ($5.2 million / $4.0 million).

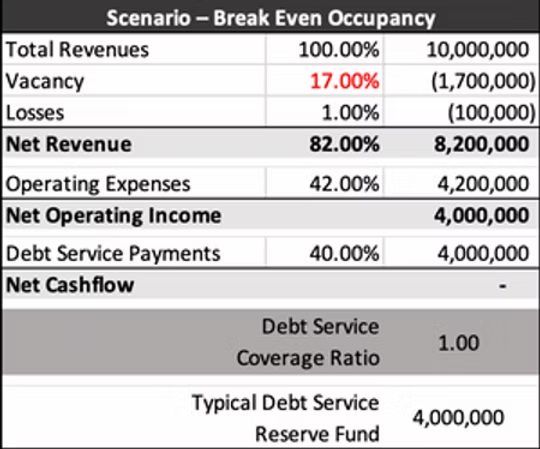

Scenario – Break-Even Occupancy

Break-even occupancy occurs when there is a 1x DSCR. If we assume that losses and operating expenses remain constant, we can solve for the level of vacancy that leads to a 1.0x DSCR. In the simplified example, this level of vacancy is 17%, which implies an 83% occupancy, or 830 students living in the project. If break-even occupancy was a University goal, the University has several options to achieve break-even occupancy at the lowest possible density. The specific arrangements would depend on the specific layout of the rooms and the associated common space but, for this example, there is not a scenario where all students can occupy individual living spaces with break-even occupancy. We are able to get close, but only if the quad units are considered to have individual living spaces and single students are placed in each double room. This would allow for 800 students, but requires 400 students to share the common living room spaces in their quads.

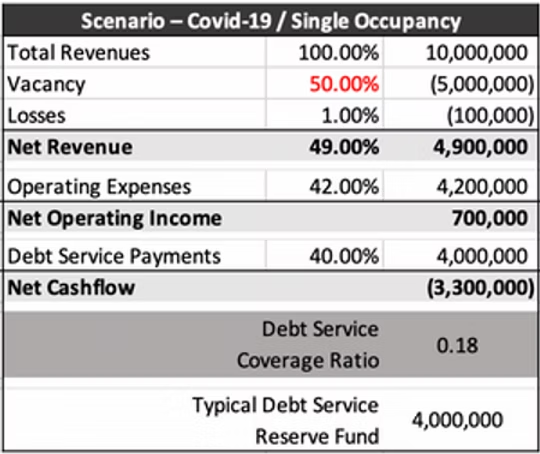

Scenario – COVID-19 / Single Occupancy

If in response to COVID-19 the University decided that the risk of an on-campus outbreak is best minimized through single occupancy of housing units, this had significant implications for the financial performance of the project. The example project has 500 units; a single student in each unit implies 50% occupancy and a reduction of net operating income to $700,000. Net operating income of $700,000 is substantially below the required debt service payment of $4 million. If University financial support was not feasible due to other budgetary limitations, the project drew upon reserve funds – the debt service reserve fund, in our example – to make the $4.0 million debt service payment.

Long-term Implications: Most P3 housing deals are structured such that reserve funds, such as the debt service reserve funds, have to be replenished to specified levels before any form of distributions can be made. The result of this requirement is that even if housing operations return to “normal” in subsequent years, the University would not receive “normal” distributions for several years, as reserve funds are replenished. In the example, normal distributions would not return for least 3 years ($3.3 million / $1.2 million = 2.75 years), as revenue is first diverted into the debt service reserve fund.

As demonstrated above, these low-occupancy scenarios cause higher education institutions to make wrenching decisions to minimize the financial impact from P3 housing projects in crisis. As we continue to work through and manage the COIVD-19 pandemic, we expect that for many universities the pandemic will leave lasting scars on university housing operations.

Contact Us!

Contact Johan Rosenberg [email protected] or Justin Krieg at [email protected] to learn more, or if your project is facing financial difficulty.

Media:

Megan Roth

952-746-6050