Higher Education Rating Agency Medians – Some Stabilization in FY 2023, but Enrollment and Operational Challenges Remain

In fiscal 2023, the sunsetting of federal pandemic relief aid and growing inflationary pressures weighed on public and private universities alike, pressuring operations and driving margins down to pre-pandemic levels or below. Enrollment challenges persisted for both public and private institutions, with a growing disconnect between larger, higher-credit-quality institutions and smaller, more regional entities with greater exposure to demographic pressures and fewer options to alleviate them. Despite these headwinds, there were also positives for the sector, with balance sheets remaining stable after investment losses in FY 2022 and capital spending up modestly for both publics and privates. For publics, operational pressures were counterbalanced by a favorable state funding environment, with increased state appropriations in many states buoying performance and providing a stabilizing source of revenue beyond student-derived tuition, fees, and auxiliaries. Overall, while the metrics shown by the rating agencies indicate that the higher education sector weathered the first “full” post-pandemic year with reasonable success, Moody’s, S&P, and Fitch all expect to see persistent challenges facing these institutions in the years ahead.

Operating Performance Softens Across Sector, Though Rising State Support Provides a Buffer for Publics

With federal pandemic-related aid rolling off almost entirely in FY 2023, all three major rating agencies saw dips in operating performance and margins for rated higher education borrowers to levels more commensurate with pre-COVID results. Decreased operating margins were exacerbated by inflationary pressures and increased expenses. Indeed, Moody’s saw overall growth in revenue for both public and private medians (3.8% and 2.3% sector-wide growth, respectively), but not enough to outweigh corresponding expense increases. S&P and Fitch also saw similar declines in operating margins. S&P’s median sector-wide operating margins for publics and privates fell to 0.3% and -0.1% (from 2.9% and 1.1% in FY 2022, respectively). This marks the first time in over a decade that the median operating margin for privates was negative. Fitch’s rated publics and privates exhibited similar trends, with the rating agency anticipating that pressure on cash flows and operations is likely to continue given a murky enrollment picture and evolving economic environment.

For public universities, however, increased state funding provided a welcome steadying factor for operating performance given the other challenges facing the sector. Moody’s indicated that over half of their rated publics saw state appropriations per student increase by 9% or more in FY 2023, and state appropriations per FTE (“full time equivalent”) increased across S&P’s rated universe of publics by 11.6%. Although growth in appropriations has not been, and isn’t expected to be, perfectly consistent across all states (with S&P noting cuts to higher education budgets in Arizona and California announced for FY 2025), rating agencies expect continued strong support from state governments overall. Such support will continue to increase revenue diversity for publics while helping to ease expense and demand-based pressures on operating performance.

Relative Enrollment Stability, But Lower-Rated Universities Face Greater Pressures

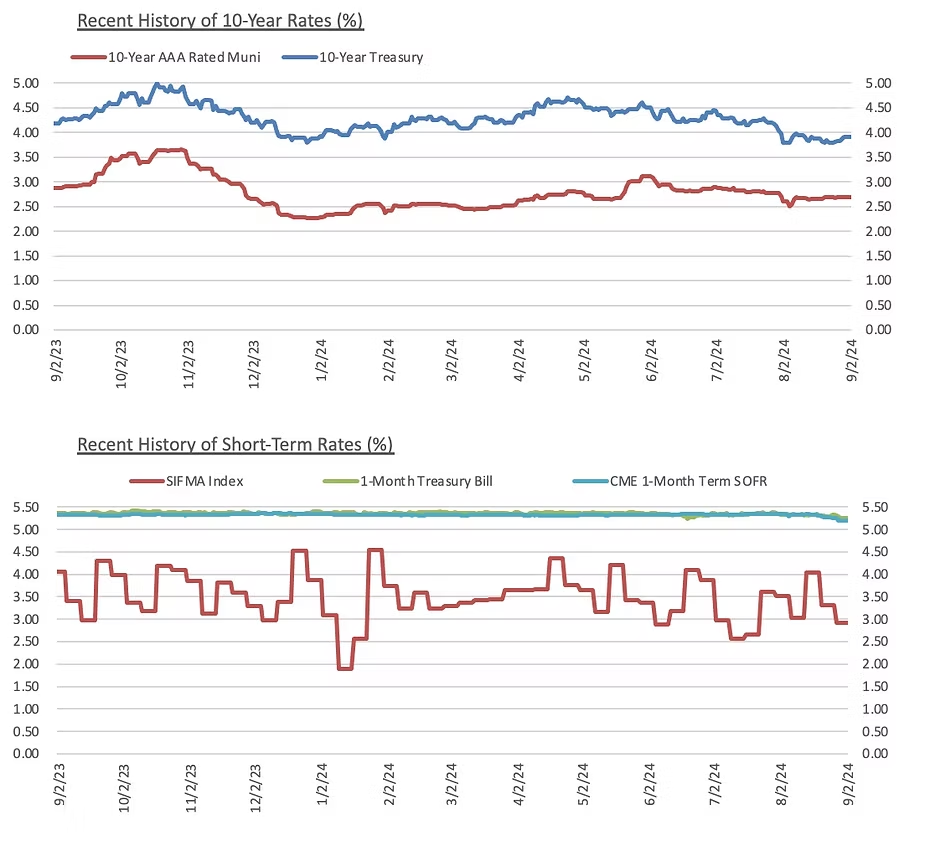

The Federal Reserve’s fight against inflation and its impact on markets and the broader economy remain key issues. In recent weeks, we have seen encouraging data suggesting that inflation is finally falling back toward the Fed’s long-term 2% target. In June, the core personal consumption expenditures price index, the Fed’s preferred inflation gauge, increased 0.2% and was up 2.6% from a year ago. A jobs report released earlier this month showed unemployment rising to 4.1%, slightly higher than the 4% target set by the Fed. Debt and equity markets have been reacting favorably to the news. According to the CME Group, as of July 30 there is now a 100% probability of a rate cut on or before the September 18th meeting. 85.8% of respondents believe there will be a 25 bps cut, while just under 14% of respondents believe it will be a 50 bps cut. Many of those respondents think further cuts will be in store before the end of the year. As of July 30, ~57% of those surveyed believe the fed funds rate will be in the 450-475 bps range following the December 18 meeting.

As we move further into the second half of 2024, we are cautiously optimistic that these favorable trends will continue. If the market’s expectations of the Fed hold true, rates could ease further as the summer and fall progress. We expect to see some volatility in the markets around the election in November, which is not unusual. A change in presidential candidates a few months before the election introduces another layer of uncertainty around how markets will react to the new administration. If inflation and unemployment data continue to move in the right direction, however, this volatility may be short-lived. If you have questions or would like to discuss capital plans in the context of these market conditions, please schedule some time to connect with your Blue Rose Advisor.

Wealth Levels Remain Stable, With Market Factors Driving Capital Spending and Reduced Debt

After much of the sector experienced investment losses in FY 2022, FY 2023 was a welcome return to stability for the balance sheets of higher education borrowers. While the massive gains of FY 2021 were not replicable, modest growth of investments provided stability for issuers, and most balance sheet ratios improved from the combination of this resource growth and light debt issuance, causing debt levels across the sector to remain flat or even decline slightly. Both S&P and Fitch credited higher interest rates as a major factor influencing borrowers to borrow less, particularly given many institutions had previously taken advantage of much lower rates during the pandemic to issue low-cost debt. Interestingly, capital spending increased slightly for publics and privates alike even with reduced debt issuance, as universities continue to face pressure to modernize and maintain their campuses to attract students. Despite this small increase, all three rating agencies expressed varying versions of the same point – capital spending remains comparatively low overall, and further expenditures will almost certainly be required over the coming years to keep age of plant in check and allow schools to achieve their strategic goals.

As a whole, fiscal 2023 was a relatively soft landing for the higher education sector given the sudden loss of federal relief aid and the varying inflationary, COVID-induced, and demographic pressures exerting themselves on universities. This stabilization can be seen across the rating agency medians, but pressure points remain apparent beneath the surface, as lower-rated, smaller, and more regionally focused institutions face far greater challenges than large, comprehensive institutions with a national reach. As such, it remains imperative for university leadership to be ever mindful of the pressures facing the sector and plan for how best to adjust to those pressures in the years to come. If you have questions about the current credit environment for higher education and how your institution can plan to navigate it, we encourage you to reach out to your Blue Rose advisor.