Since we published our 2020 Mid-Year Market Update last June, the financial markets have calmed down from the historic turbulence experienced as a result of the COVID-19 pandemic. Two topics have come to the forefront of current municipal market discussion: the changing rate environment, and the continued efforts to transition from LIBOR to SOFR.

Changing Rate Environment

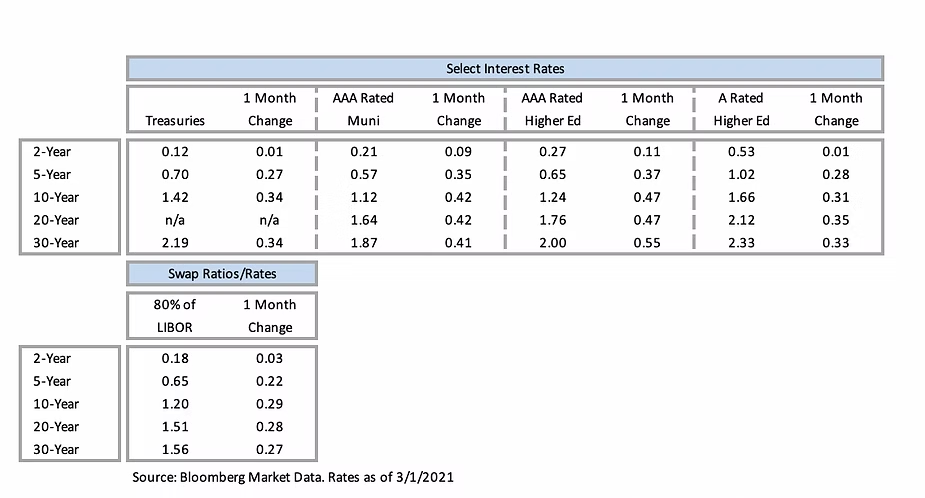

The primary market mover in 2020 was the COVID-19 pandemic (our April and June editions of The Shield touched on this impact), with significant federal stimulus helping reverse the negative market trends that resulted. Currently, absolute interest rates remain low despite some recent steepening. Overall, the market environment remains relatively attractive to borrowers as credit spreads have managed to creep downward through the start of 2021; primarily driven by higher investor demand compared to a lower supply.

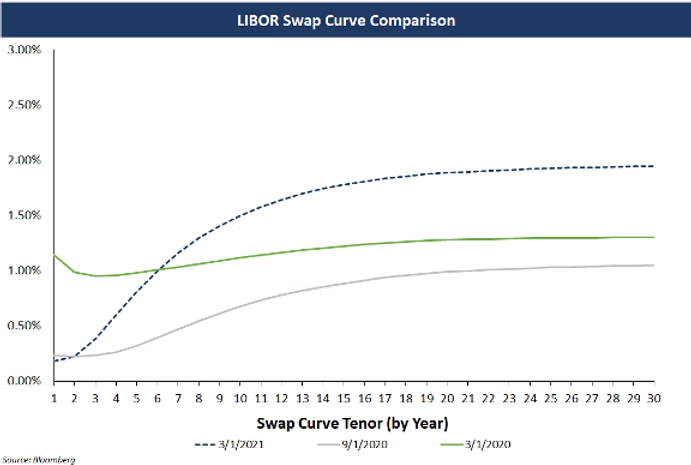

MMD:

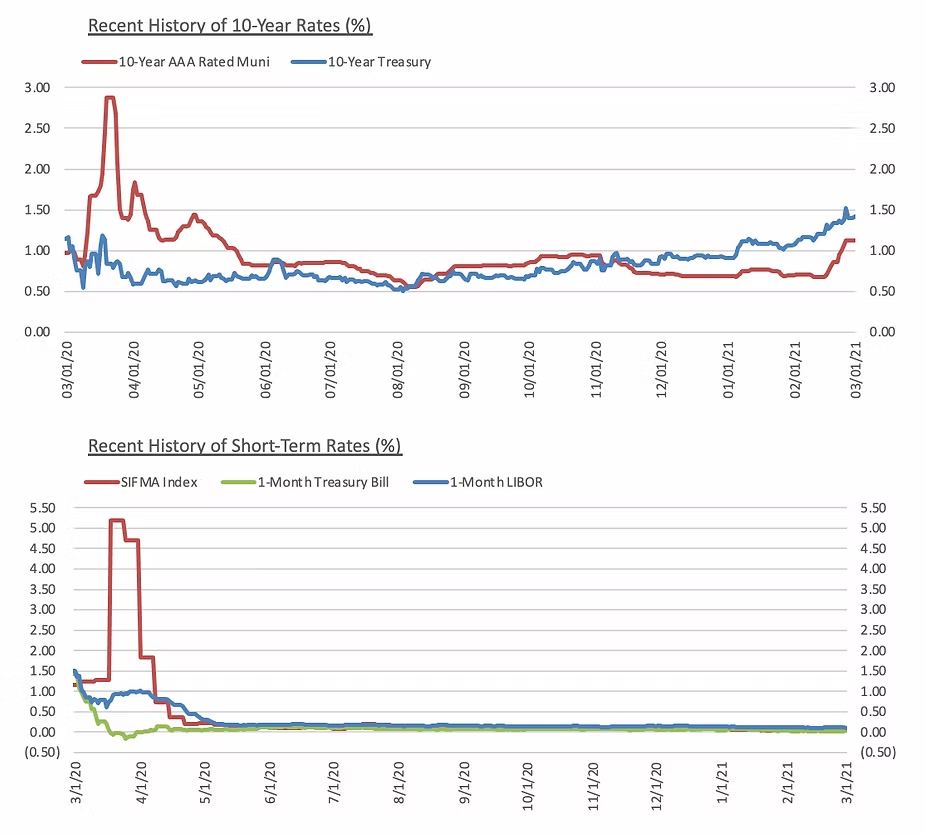

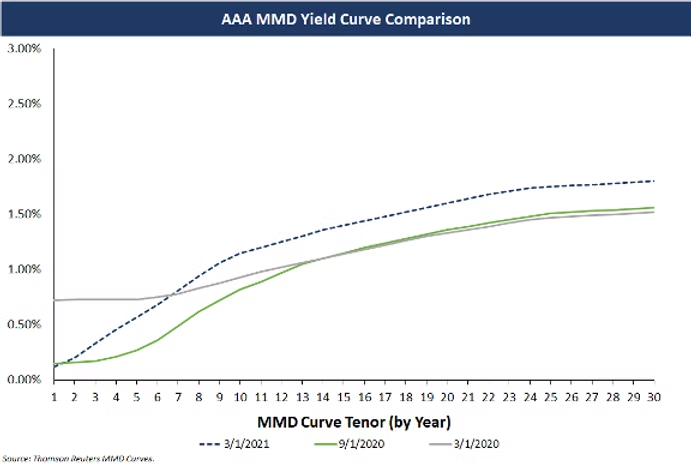

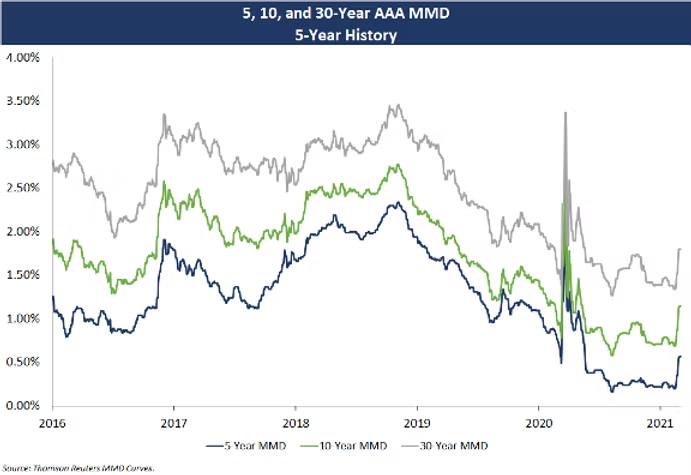

Over the past year, MMD levels have remained near historic lows, with a steepening trend that followed the start of the COVID-19 pandemic.

The significant volatility experienced by the MMD index in the immediate aftermath of the pandemic has continued to stabilize, though rates have increased significantly over the past few weeks following a significant upward move in treasuries (primarily based on an improved economic outlook).

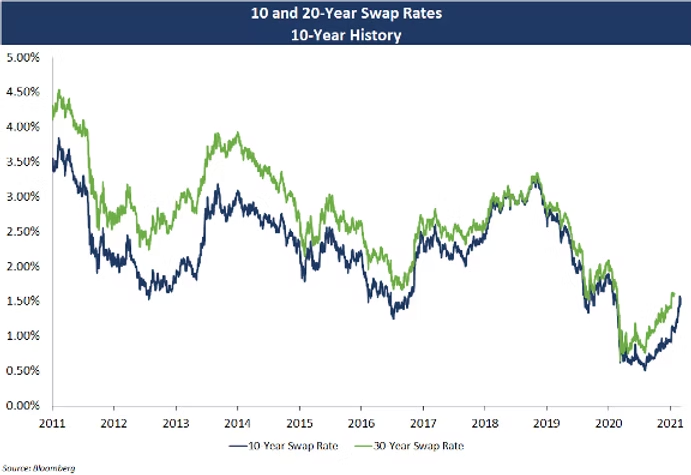

LIBOR:

Consistent with the steepening trend is the LIBOR index, whose rates remain historically low, particularly on the short end of the curve.

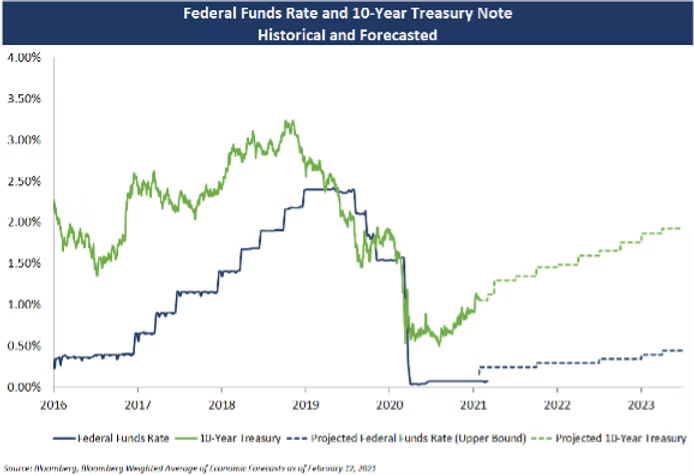

Fed Funds:

In August of 2020, the FOMC announced significant changes to its target view of U.S. employment and inflation. At the January Fed meeting, Jerome Powell indicated that there is still work to be done to recover employment levels, expressing less concern about increased inflation in the current economy. The Fed’s overnight target rate fell off a cliff as part of its response to the COVID-19 pandemic, with a target range of 0%-0.25% announced in early March of 2020.

Since then, the Fed has indicated that it does not plan to target rate hikes in the foreseeable future, with the expectation being to maintain its current target range until at least 2023.

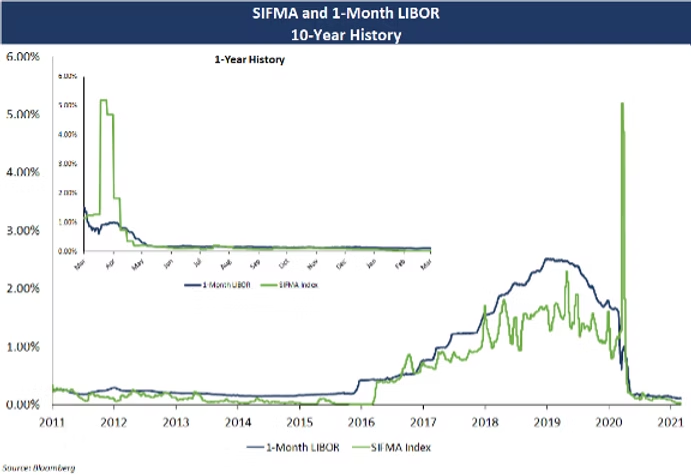

SIFMA/LIBOR:

As a result of Fed action to stabilize the broader markets, the VRDB market and the SIFMA/LIBOR relationship has continued to stabilize. Both indices have remained at very low levels (near or below 0.10%).

LIBOR Transition

The LIBOR transition process continues, while milestones set by the ARRC (Alternative Reference Rate Committee) continue to be met on time (https://www.newyorkfed.org/arrc/sofr-transition#pacedtransition). Importantly, the deadline for transition has shifted over the last three months, with Banks now expected to no longer be obligated to make LIBOR submissions after June 30, 2023, an 18-month extension from the initial LIBOR cessation date.

To better address the impact of regulatory announcements and changes to the timing of the transition, Blue Rose, along with our affiliate company HedgeStar, is hosting a webinar on March 18th at 1:00 pm CST.

Additional Resources

For further detail on this topic, the ARRC continues to publish major updates on its website (https://www.newyorkfed.org/arrc/sofr-transition#progress).

About the Author:

Webinar: LIBOR Transition – Be Prepared!

March 18, 2021 1:00 pm – 2:00 pm CST

In this session, we are focusing on the inevitable transition from the London Interbank Offered Rate (“LIBOR”) to the Secured Overnight Financing Rate (“SOFR”) from a borrower’s perspective. We address SOFR “math” with insight into the mechanics of the transition and answer the question plaguing so many on this subject – what should I do next?

How did we get here? We will begin with a brief history on LIBOR and the current transition timetable from the Alternative Reference Rate Committee. The presentation will continue with a deeper understanding of SOFR and the economics surrounding the LIBOR-SOFR transition related to loans and derivatives. Importantly, we will discuss some of the perceived shortcomings of SOFR and alternatives being considered by market participants. Might there be market opportunities ahead of a formal conversion? Finally, we will conclude with the “do’s and don’ts” of transition preparation and hedge accounting considerations.

Key Objectives & Key Take-Aways:

Understand the reason for LIBOR cessation and the mechanics of SOFR.

Learn about SOFR and where it is and isn’t an appropriate replacement index.

Understand how the value of your portfolio might be impacted by the transition.

Identify the action items in preparation for an ultimate transition.

Level: Basic

Advanced Preparation: None

Prerequisites: None

Field of Study: Finance

CPE Credit(s): 1

Delivery Method: Group Live

Cost: FREE

Comparable Issues Commentary

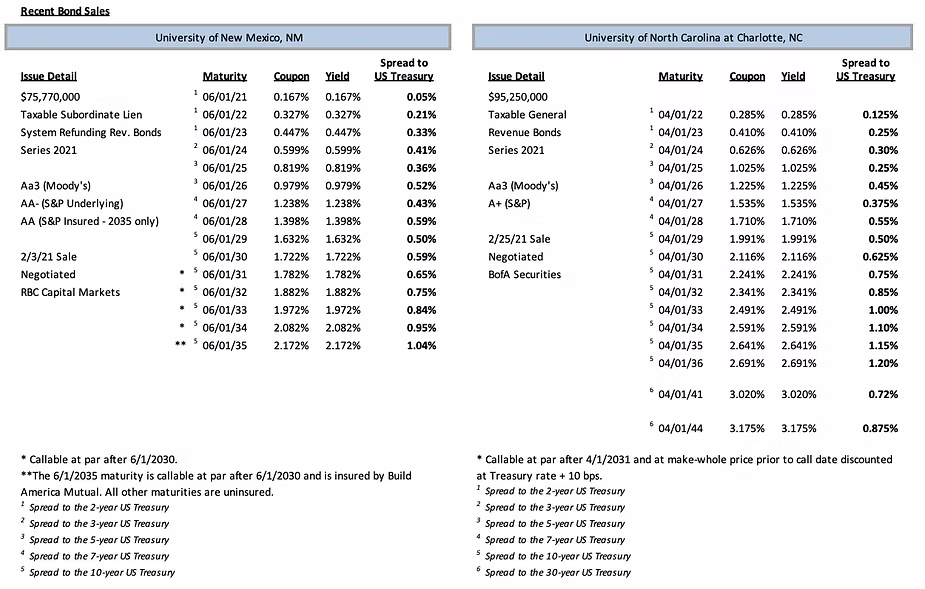

The two schools priced into a market with credit spreads continuing to tighten relative to 2020’s COVID-inflated levels, but one that also saw taxable indices rising markedly during the month of February. For reference, the 5, 7, 10, and 30-year treasuries all increased by 35-40 bps between UNM’s pricing on February 3rd and UNC Charlotte’s bond sale just over 3 weeks later on February 25th. The two transactions priced relatively similarly on a spread basis, with most comparable maturities spread within ~10 bps of one another – UNC Charlotte priced tighter on the front end of the curve and New Mexico achieved lower spreads on later maturities from 2030-2035. However, the massive shift in taxable benchmark rates resulted in UNC Charlotte’s absolute yields exceeding those of New Mexico by over 50 bps for some later maturities, though the shortest part of the yield curve (1-3 years) remained relatively stable between the two pricings. Both universities sold their bonds with par call features, with UNM utilizing a 9-year call in 2030 while UNC Charlotte opted for a standard 10-year par call in 2031 (UNC Charlotte, unlike UNM, also issued its bonds with a make-whole call option prior to the par call date). The bonds were each serialized at least through 2035 (the final maturity of New Mexico’s Series 2021 issue), with UNC Charlotte’s longer-dated final maturity resulting in the use of two term bonds in 2041 and 2044.

Interest Rates